Auto insurance policies are confusing and boring documents filled with legal jargon that can be an absolute nightmare to read. Your policy is a legal contract binding the insurance company to perform specific actions under certain circumstances for an agreed upon price. Insurers want the contract to be as specific as possible, which is why policies are so detailed and written in legalese.

Resist the temptation to gloss over your insurance, because understanding your insurance policy can help avoid costly coverage gaps or frustration with your insurer after an accident. As the saying goes: an ounce of prevention is worth a pound of cure.

Review the declaration page

The declaration page is arguably the most important page of your policy, but it shouldn’t be the only page you read.

“The declaration page ‘declares’ what coverages you have elected to have on your policy and which you have declined,” explains Carole Walker with the Rocky Mountain Insurance Information Association. “It also includes details about coverage levels, deductions, named drivers and the price you are paying for each coverage.”

The declaration page should be the first page and clearly labeled as “your policy declarations” or “declarations page.”

With many car insurance companies, you don’t have to wait for a paper copy to arrive; you can log in and view your policy online.

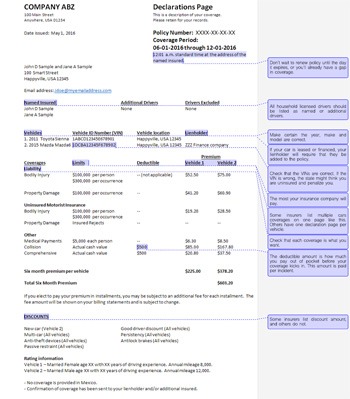

Information included on the declaration page includes:

- Personal information: Your policy number and personal information, such as your address

- Insured drivers: Names of all of the drivers insured under this policy

- Insured vehicles: The vehicles insured by this policy, including the VIN numbers

- Schedule of coverages: A listing of the coverages, limits, deductibles and the premium for each coverage. This should be broken out by vehicle if you have multiple vehicles on your policy. If a coverage is not listed in this section, you don’t have it.

- Policy period: The dates the policy is in effect

- Discounts: Any discounts that have been applied to the policy

- Surcharges: If you’ve received a speeding ticket, or made a recent claim there will be a surcharge on your premium.

While it is termed a declaration “page,” it may be double-sided or multiple pages, so be sure to read it in its entirety.

KEY TAKEAWAYS

- The declaration page tells what coverage you have on your policy and which you have declined.

- You will find a definitions section and the details like who is insured, what is insured, and when it is insured, mentioned in your auto insurance policy.

- When you make changes to your policy, like adding or removing a car or driver, the company will send you a new declaration page.

- If you find that you have gaps in your insurance or are underinsured, it is time to start shopping for more coverage.

Review after changes and renewals

When you make changes to your policy, such as adding or removing a car or driver, you should be sent a new declarations page that shows the alterations to your policy.

If you don’t receive a new one within a week after the change, call your insurance company:

- Confirm the policy changes were made

- Request that your carrier send you a new declarations page showing the changes

“It’s imperative that this page be reviewed at each renewal to ensure everything is accurate and the basic details have not changed,” warns Paul Dreher with Lawley Insurance in Buffalo, New York.

| Ultimate Insurance

| Get a Quote |

| Pretected

| Get a Quote |

Coverage levels

Choosing the proper coverages and levels is one of the most important parts of car insurance. Without the proper coverage, you may be responsible for damages.

“It’s very important to have enough liability insurance, because if you’re involved in a serious accident, you may be sued,” advises Loretta Worters, vice president of communications with the Insurance Information Institute.

Here is a rundown of the various coverages and recommended levels:

- Liability: This coverage pays medical bills, legal settlements, and repairs that are the result of injuries or damage that you or a designated driver cause to someone else’s person or property. It will also protect you when driving someone else’s car with his or her permission. This coverage is required in almost all states, but required liability coverage levels vary by state. Liability insurance is broken down into three amounts: per person limit for bodily injury, per incident limit for bodily injury, and a property damage limit. Using the recommended amounts of $100,000, $300,000 and $100,000, the limits are generally written as 100/300/100.

- Collision: This coverage pays for any damage to your car resulting from a collision with another car or object, regardless of whether you are at fault. Deductibles generally range from $250 up to $1,000. Typically, a higher deductible means a lower premium.

- Comprehensive: This insurance will pay for damage to your vehicle that is caused by theft or something other than a collision. Covered perils include fire, falling objects, explosions, earthquake, windstorms, hail, flood, vandalism, riot, or contact with animals, such as deer. It also covers damaged windshields and other glass damage. Like collision coverage, you can choose your deductible amount. Your options normally range from $100 to $1,000.

- Medical Payments or Personal Injury Protection (PIP): This will pay for the medical treatment of the policyholder and any passengers in the vehicle that were injured during an auto accident, regardless of fault. PIP may cover lost wages and funeral costs. Requirements for this coverage vary by state.

- Uninsured and Underinsured Motorist Coverage: This will pay for damages if you, a family member or a designated driver are hit by a driver who is uninsured or underinsured. Requirements for this coverage vary by state. In states where the coverage must be offered but can be rejected, your declarations page should note “insured rejects” if you have waived the coverage.

QuickTake

Sample declaration page

Click here to zoom in

This is an example of a typical declaration page, highlighting specific details that you should review as you read through your policy. Click to enlarge the sample page.

Policy terms can be confusing

Because insurance policies are written in legal language, they can be confusing. All policies have a “Definitions” section that defines specific words used in the policy.

“The ‘Definitions’ section is extremely important as the terms contained there will define who is insured, what is insured, and when it is insured. You will need to refer back to the definition page often,” advises Kristofer Kirchen, with Advanced Insurance Managers.

Defined words will be bolded in the policy. Here are a few key terms:

- Family member: Take note of what is considered a family member or insured driver.

“Ideally this should read ‘an or any insured’ which is a broad definition, not ‘the insured’ which is a much more narrow definition,” warns Amy Bach with United Policyholders.

If your policy only notes “the insured” or “named insured” under the coverages section, you have a restrictive policy that does not extend coverages to those who are not specifically listed on the policy. This means your vehicle isn’t protected if a relative borrows your car and gets into an accident.

- Covered autos: Some policies may not cover damage to “substitute vehicles,” which would include a loaner or rental car.

- Actual cash value (ACV): Collision and comprehensive policies usually pay out the actual cash value, which means that the insurance company will determine the market value of the car at the time of loss. If the car is newer, this amount may be less than you owe on the vehicle, as new cars depreciate quickly. Gap insurance could prevent a large discrepancy in the amount you owe compared to the amount you receive.

- After-market parts: These are parts made by a company other than the auto manufacturer. You can add an original equipment manufacturer (OEM) endorsement to your policy so only OEM parts are used to repair your vehicle – but you’ll pay more for this option. For example, if your classic car was damaged in an accident, the allotment for OEM parts would be used in the repairs.

Keep an eye out for words and phrases such as “does not apply to,” “except,” “all,” and “however.” These words can proceed or follow coverage explanations and drastically change the meaning.

If you discover words you don’t understand, check the definitions page or contact your insurer for clarification.

Read the insuring agreement

Car insurance policies will have an insuring agreement for each coverage type: liability, uninsured/underinsured, medical/PIP and collision and comprehensive.

“The insuring agreement is the actual binding contract that governs whether or not coverage is afforded in the event of a loss,” explains Kirchen. It defines what is covered and how it is covered.

Here are a couple of tips from Kirchen about reading your policy:

- If the policy refers to another section when describing coverage, read the referred to section immediately to ensure there are no exclusions.

- Pay particular attention to the exclusions in each section and the exclusions that apply to the policy as a whole. Exclusions can have a major impact on a claim.

Items listed on your policy as an “exclusion” are not covered. Common exclusions include the following examples, with a note of what section of the policy they are considered:

- Intentional damage to others, bodily injury or property damage (liability)

- Property damage to your own property (liability)

- Damages caused by your vehicle being used for livery purposes (liability)

- Damages caused by using your vehicle for business purposes (liability)

- Intentional damage to your own vehicle (collision and comprehensive)

- Damage done to your vehicle by war, bio-chemical attack, nuclear exposure (collision and comprehensive)

- Personal items that are not permanently installed in your insured vehicle (collision and comprehensive)

- Any vehicle used for competing in any prearranged or organized racing or speed contest (liability, plus collision and comprehensive)

If you have a restrictive policy, there may be many more exclusions, such as not allowing permissive drivers or extending coverage to rental vehicles.

Insurance experts say…

The world of car insurance is filled with pitfalls that can leave you unprotected. Here are a few things to be aware of when shopping for coverage:

Minimum coverage is not enough.

Meeting the state requirement is one thing, but having enough coverage to cover the cost of a new car, medical bills or a lawsuit is quite another. In California, the minimum required property liability coverage is $5,000. In 2015, the average cost of a new car was around $33,000. If you were at fault for totaling the other driver’s brand-new vehicle, you’d be stuck paying the $28,000 out of pocket.

“A major mistake that many consumers make is opting for the minimum state required coverage,” warns Worters. ”The minimum coverage for bodily injury may be as low as $10,000 per person. In today’s litigious society, that is not enough.”

“You should carry enough liability to protect your assets in the event of an accident. It’s possible to get additional coverage with a Personal Umbrella or Personal Excess Liability policy,” advises Worters.

Double the coverage isn’t double the price.

Carrying more coverage than the state minimums is not as unaffordable as you think – especially compared to the $28,000 price tag of the accident in the example above.

“In many situations, the cost to dramatically increase your coverage can be less than $100 per year,” advises Dreher.

In fact, the national average to increase liability coverages from state minimum to 50/100/50 is around $67.

Your old car probably doesn’t need collision and comprehensive.

If you have a vehicle you would replace it instead of repairing it after an accident, consider dropping collision and comprehensive. Typically, if the car is over 10 years old, the vehicle’s value no longer makes the cost of the coverages worth it. For example, if your car is worth $3,000 and your deductible is $500, your potential payoff is $2,500. If your annual comp and collision premiums surpass 10 percent of the payoff, in this case $250, consider cancelling the coverage to save for a newer car.

Be aware of your credit report and score.

If you aren’t up to date on your credit report and credit score, there’s no time like the present.

“Your credit score and personal data impact your premium now more than ever,” warns Bach. “It’s important to make sure your insurer is basing your premium on accurate information about you and your credit.”

Personal finance experts advise paying for your three FICO credit scores once a year. You can access your free TransUnion credit score and report through Wisepiggy.com. Keeping this information accurate and resolving any incorrect information or identity fraud helps to secure the best rates.

Assess your coverage needs every few years.

Whether buying a new car or having a baby, your personal assets change and grow over time and protecting them with insurance is critical. “It’s important to review coverage options and become educated about the importance of adequate limits to protect your assets and future earnings,” advises Dreher.

Consider these questions and talk to your insurance agent or a financial advisor to make sure you are fully protected:

- Have you acquired any assets that need protection since you established your policy, like purchasing a house or receiving an inheritance?

- Would your current insurance coverage protect you and your family in a major accident?

- Would your property damage liability cover the cost of a newer car if you damaged a person’s vehicle in an accident?

Insurance is complicated, so turning to an expert is a great idea if you have questions or trouble understanding your policy.

“Ultimately, the best advice is to speak with your agent in the event that you do not understand some of the verbiage or how the policy responds in a given circumstance. Be sure to do the reading and ask those questions before you have a loss,” says Kirchen.

Review your policy now

Take the time to honestly and realistically assess your assets and the protection offered by your current insurance policies.

If you find gaps or discover you are underinsured, it’s time to start shopping your coverage. Even if you feel good about your coverage levels, shopping around may result in some savings. Insurers rate risk differently, so premium quotes can vary dramatically.