Covered California is the state’s health insurance exchanges, which the Affordable Care Act (ACA) created. The exchanges help connect people to individual and nongroup health insurance.

These plans offer comprehensive coverage and provide discounted rates for people based on income.

Covered California differs from most states in two major ways:

- All Californians need health insurance. The state has an individual mandate that requires that people have health insurance. If you don’t have coverage, you’ll get fined at tax time.

- The state has expanded subsidies to help middle-class people pay for their health care. The expanded subsidies lower health insurance costs for more than 1 million people.

KEY TAKEAWAYS

- Covered California is the state’s individual marketplace where people can find individual health insurance.

- California residents, as well as undocumented people are eligible to get Covered California plans.

- The open enrollment for Covered California runs from November 1-January 31. You can sign up or make changes to your health plan within these three months.

- Covered California also offers dental plans and these are separate from health insurance plans.

Now let’s dive into Covered California, the types of plans, who’s eligible, how to enroll and how to save via subsidies.

What is Covered California?

Covered California is the state’s individual marketplace. The ACA created individual marketplaces, which help people find individual health insurance. You may need individual health insurance if your employer doesn’t offer coverage or the plans are too expensive or limited.

Covered California enrolls 1.5 million people in health insurance plans.

Covered California plans must offer 10 essential health benefits. That’s required in the ACA.

The 10 essential health benefits are:

- Outpatient services

- Emergency services

- Hospitalization

- Pregnancy, maternity and newborn care

- Mental health and substance abuse care

- Prescription drugs

- Rehab and habilitative services and devices

- Labs

- Preventive and wellness and chronic disease management

- Pediatric services, including oral and vision care

Types of Covered California plans

Similar to other health insurance exchanges, Covered California classifies its plans based on costs. Each plan gets a metal classification that gives you an idea about premiums and out-of-pocket costs.

Here are the differences:

| Type of plan | % of health care costs that plan pays | % of health care costs that member pays | Premiums | Out-of-pocket costs |

| Bronze | 60% | 40% | Lowest premiums | Highest out-of-pocket costs |

| Silver | 70% | 30% | Lower than Gold, higher than Bronze | Higher than Gold, less than Bronze |

| Gold | 80% | 20% | Lower than Platinum, higher than Silver | Higher than Platinum, less than Silver |

| Platinum | 90% | 10% | Highest premiums | Lowest out-of-pocket costs |

Beyond the metal plan, you can choose the type based on plan design. While the metal classification varies by costs, the plan design dives deeper into the care. Here are the types of health plans offered:

- Preferred provider organization (PPO) — PPOs offer large provider networks and let you receive out-of-network care. You’ll have to pay more for that care, but out-of-network care is an option — unlike other types of plans. PPOs don’t require referrals to see specialists. PPOs usually have higher premiums than other plans for the flexibility of going out-of-network and not needing referrals.

- Health maintenance organization (HMO) — HMOs offer restricted provider networks and you need to get referrals from your primary care provider to see specialists. You can’t usually get care outside of your network. If you see a provider outside of the network, you may have to pay the whole bill with no help from your plan. These plans have lower premiums than PPOs.

- Exclusive provider organization (EPO) — EPOs are a PPO/HMO hybrid. EPOs don’t require you to choose a primary care provider. You don’t need referrals to see specialists. So, in those cases, it’s like a PPO. However, similar to an HMO, EPOs have restricted networks and won’t pay for care outside of your network.

- Healthcare service plan (HSP) — HSPs are similar to EPOs. HSPs require that you name a primary care physician and there’s no out-of-network care. In those ways, HSPs are like HMOs. However, you don’t need a referral to see specialists if you have an HSP, which is similar to a PPO.

People looking for a plan through Covered California usually have multiple choices. Covered California said that nearly all Californians have at least two health insurance company options in 2020. Seventh-seven percent have at least four insurer choices.

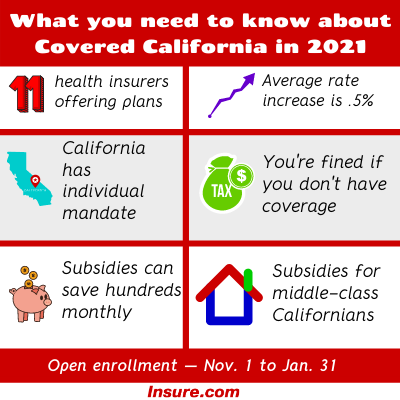

Eleven insurers will again provide plans in 2021. Here are the insurers and the weighted average rate change for 2021:

- Anthem Blue Cross of California — 6%

- Blue Shield of California — -2.4%

- Chinese Community Health Plan — -1.3%

- Health Net — 2.8%

- Kaiser Permanente — 1%

- L.A. Care Health Plan — -4.6%

- Molina Healthcare — -3.8%

- Oscar Health Plan of California — 7.6%

- Sharp Health Plan — -0.5%

- Valley Health Plan — 9%

- Western Health Advantage — -2.6%

In addition to health insurance, Covered California offers dental plans. These are separate from health insurance plans. Insurers with dental plans are:

- Access Dental Plan

- Anthem Blue Cross

- California Dental Network

- Delta Dental of California

- Dental Health Services

- Liberty Dental Plan

- Premier Access

Covered California offers two dental plan designs: HMOs and PPOs.

| NextGen

| Get a Quote |

| HealthPlanRate.com

| Get a Quote |

| HealthCare.com

| Get a Quote |

| Short Term Plans

| Get a Quote |

| Medicare Providers

| Get a Quote |

Individual mandate in California

California has an individual mandate that requires most Californians to have health insurance. The ACA implemented the individual mandate on a federal level. Congress has since removed the individual mandate fine, but the Golden State implemented it at the state level starting in 2020. There are a handful of states with their own individual mandate.

You’ll get fined at tax time depending on your family size and income if you didn’t have health insurance coverage in the previous year. The penalty is $750 for uninsured adults and $375 for uninsured dependent children under 18. So, a couple with two children would pay a $2,250 penalty at tax time if they don’t have health insurance.

Who’s eligible for Covered California?

Calfornia residents, as well as undocumented people, can apply for Covered California plans.

During the application process, Covered California will verify your identity, income, citizenship and immigration status. If Covered California can’t confirm any information, the state may deem you “conditionally eligible.” In that case, you’ll get coverage for 90 days while you provide additional documents to Covered California.

Stimulus package lowers costs of Covered California plans

The American Rescue Plan of 2021, also known as the stimulus package, included provisions to help lower health insurance costs.

The stimulus bill loosened restrictions on who’s eligible for ACA plan subsidies. Previously, people had to have a household income of below 600% of the federal poverty level in California to qualify for lower costs.

The stimulus bill removed that level and instead placed a cap. So, through 2022, people with a Covered California plan will pay only as much as 8.5% of their income on plan premiums regardless of household income. Even before the change in the stimulus bill, Covered California estimated that nearly 90% of people with a Covered California plan received subsidies to lower health plan costs.

Covered California estimates the stimulus bill will provide more than $3 billion to help Californians lower Covered California insurance costs until the end of 2022.

How much can you save? Covered California said:

- Half of the people enrolled in a Covered California plan can now find a health plan for $50 or less a month.

- On average, a 45-year-old couple earning $80,000 with two children can save $1,500 per month through subsidies.

“Many people who enroll through Covered California will be able to find a plan for as low as $1 a month,” according to Covered California.

How to enroll in Covered California

You can apply online, in person or by phone.

It takes about 30 minutes to apply online. You’re able to save your application and finish later if needed. You’ll need the following documents to complete the enrollment:

- Social Security number

- Immigration documents for non-citizens

- Employer and income information

- Federal tax information

If you’d rather enroll at one of the Covered California storefronts, you can search for your local location.

As part of the application process, Covered California’s site helps you narrow choices. For instance, it will ask you how often you use medical services. Depending on whether how much you use medical services, Covered California will provide options that might work for you.

Covered California open enrollment

Covered California’s open enrollment runs from Nov. 1-Jan. 31. That gives you three months to sign up for a plan or make changes to your health insurance.

If you sign up by Dec. 15, your coverage begins on Jan. 1. If you sign up after Dec. 15, your plan will start later. Remember, if you don’t have health insurance in 2021, you’ll be subject to a fine at tax time.

If you have an existing plan and don’t make changes, Covered California will automatically renew your plan. However, it’s a good idea to check available plans to see if one is a better fit for you.

After open enrollment, you can only add coverage or make changes if there’s a qualifying event. For instance, if you have a child, get married or divorced, your spouse dies, you lose coverage or you move.

If you go through one of these life events, it will kick off a special enrollment period when you can sign up or make changes to your health insurance. Otherwise, you can only make changes during open enrollment.

An exception is Medi-Cal. Medi-Cal doesn’t have an open enrollment period. You can sign for Medi-Cal at any time if you’re eligible.

Also, remember, that Covered California doesn’t affect plans in the employer-sponsored market. Employers have their own open enrollment. It’s up to the business to decide on an open enrollment period.

How much does Covered California cost?

Covered California separates the state into 19 pricing regions. The regions vary on pricing and health insurance options. Covered California also offers subsidized ACA marketplace plans, which lowers your premiums.

Average premiums will increase by less than 1% in 2021 compared to 2020. That’s the second straight year of a less than 1% increase for Covered California insurers.

However, the rate increases/decreases vary by region. For instance, in 2021, five areas will see average premiums lower than in 2020, while another will see an almost 6% rate increase on average.

Make sure to shop around before deciding on a plan. The average savings for comparing policies is 7.4%, according to Covered California.

Here are the average rate increases by region. These don’t take into account subsidies that can help you decrease costs. Covered California also included the average savings you could receive by shopping around for a policy.

| Region | Counties in region | Average rate change | How much you can save by shopping around |

| 1 | Alpine, Amador, Butte, Calaveras, Coluse, Del Norte, Glenn, Humboldt, Lake, Lassen, Mendocino, Modoc, Nevada, Plumas, Shasta, Sierra, Siskiyou, Sutter, Tehama, Trinity, Tuolumne, Yuba | 2.6% | -0.4% |

| 2 | Marin, Napa, Solano, Sonoma | 2.3% | -1.8% |

| 3 | Sacramento, Placer, El Dorado, Yolo | 1.8% | -2.4% |

| 4 | San Francisco | 1.4% | -3.7% |

| 5 | Contra Costa | 1.9% | -2.6% |

| 6 | Alameda | 2.4% | -0.7% |

| 7 | Santa Clara | 5.6% | -5.5% |

| 8 | San Mateo | 2% | -2.8% |

| 9 | Monterey, San Benito, Santa Cruz | 0% | -3% |

| 10 | San Joaquin, Stanislaus, Merced, Mariposa, Tulare | 4.2% | 1.4% |

| 11 | Fresno, Kings, Madera | -0.1% | -3% |

| 12 | San Luis Obispo, Santa Barbara, Ventura | 2.3% | -2.2% |

| 13 | Mono, Inyo, Imperial | -2.6% | -4.7% |

| 14 | Kern | -0.2% | -2.8% |

| 15 | Los Angeles (northeast) | -1.1% | -10.7% |

| 16 | Los Angeles (southwest) | -2.1% | -13.4% |

| 17 | San Bernardino, Riverside | 0.4% | -9.9% |

| 18 | Orange | 0.5% | -11.5% |

| 19 | San Diego | -1.5% | -13.3% |

| State average | 0.5% | -7.4% |

Source: Covered California

Individual plans outside of Covered California

Most individual health insurance in the Golden State is through Covered California. However, you can also buy an individual plan that’s not part of the insurance exchange.

More than 1 million Californians with individual insurance buy it outside of the exchanges.

One downside is that people who get individual insurance outside of Covered California aren’t eligible for subsidies. However, if your household income is beyond 600% of the federal poverty level, you may want to check out individual insurance beyond Covered California to see if other plans might work for you.