There’s a lot to consider if you’re thinking about downsizing your house, especially in the current market, which strongly favors sellers. You may be able to sell your current place quickly, but many downsizers find themselves moving into an even more competitive market segment, bidding for the same properties as younger buyers looking for starter homes.

While you’re likely to be able to make a strong offer for a home, there’s still a lot more that goes into this decision, including how the pandemic might have affected your finances. If your savings took a hit or you got laid off and decided to retire early, for example, downsizing might have become a bigger priority for you.

Here are some key considerations for those thinking about downsizing.

5 reasons to downsize

- Economic necessity – It’s common for many older adults to be faced with unexpected medical expenses and rising home insurance premiums and utility costs. Selling your house and moving into a more affordable space is often the most practical solution.

- Health concerns – Many seniors downsize to a home where at-home care is more widely available and there are fewer everyday obstacles to contend with, such as stairs or other mobility constraints. The quality of and proximity to hospitals could be motivators, as well, along with access to public transportation, especially if driving has become an issue.

- Convenience – If you’re tired of doing all the housework that comes with a larger home, you’re not alone. A lot of retirees choose smaller homes where upkeep is less expensive and taxing.

- Relocating for retirement – If you intend to retire out of state or even out of your current city, downsizing in your new location could be part of those plans.

- Seller’s market – Even if you’re facing hardship right now, you’ll likely be able to sell your current home for top dollar. If you’ve been living there for a while, that means you’ll be in a position to walk away with a good chunk of change, enabling you to buy a smaller home and use the remainder to pay off debt or get out of a shaky financial situation.

Budgeting for a downsize

Choosing to downsize to a smaller home in retirement isn’t always purely a financial decision. Even for higher-net worth retirees, downsizing can be a practical move. A smaller home, particularly in a multi-family building or development, can be far easier to maintain than a single-family house on a sprawling property. This can be a priority for people as they age and are less physically able to take care of a larger home.

Whatever your motivation, it’s important to be honest about your finances and budget in advance. Here are some questions to ask:

1. What are you paying now? What will you pay in a downsized home?

Make a list of all the expenses associated with your current home. It should include your mortgage payment, utility bills, maintenance costs, HOA fees and anything else you pay related to housing on a monthly basis. Compare those numbers to what you expect to pay in the same categories in your next place.

If you still expect to take out a mortgage when you move, you’ll want to figure out the monthly payment for your new home — Bankrate’s mortgage calculator can help you crunch the numbers.

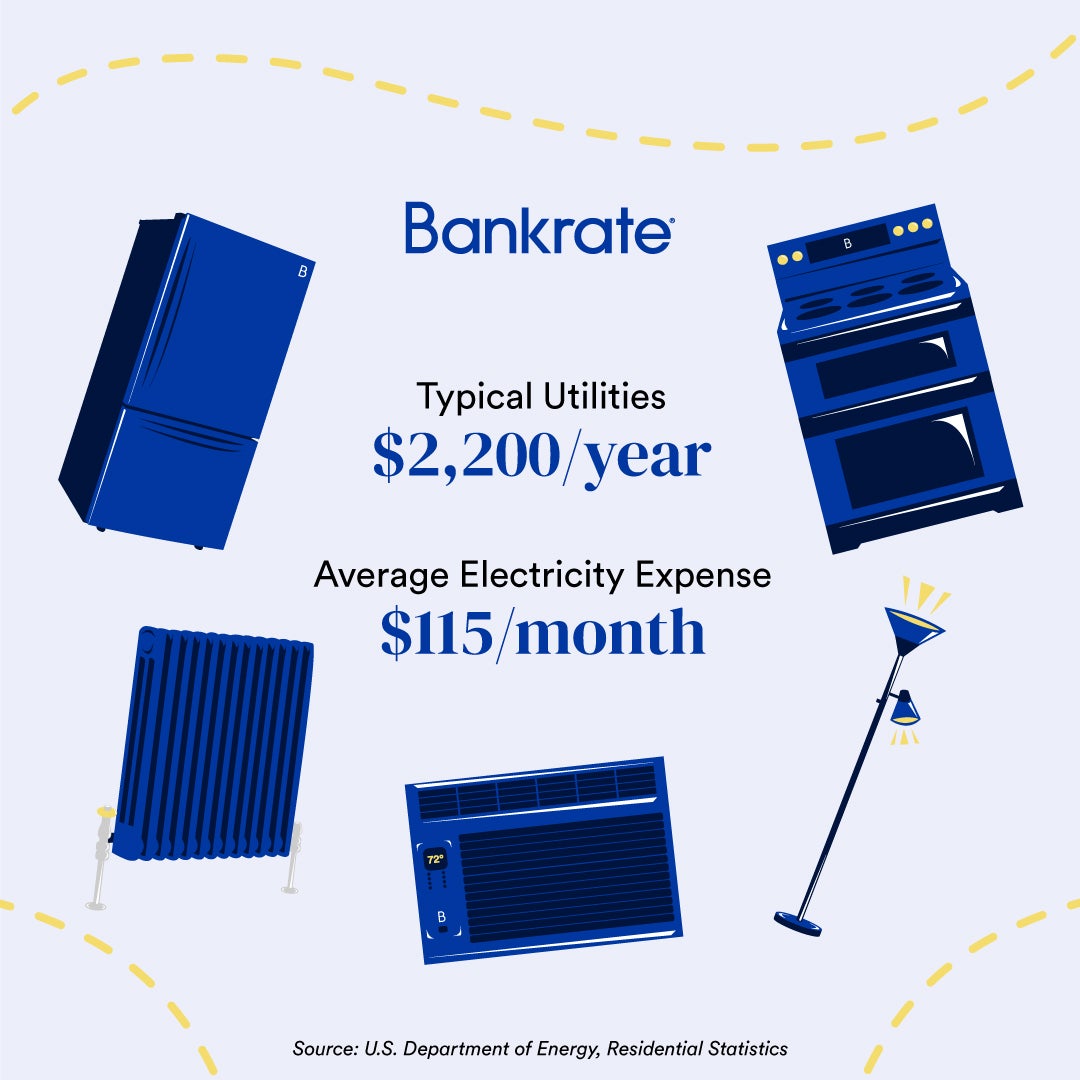

If you’re thinking about moving out of state, take a look at the U.S. Energy Information Administration’s recent data on average monthly bills for single-family homes by state. If you’re downsizing but also moving to a state where energy costs are higher, your overall savings may not be as great as you’d hoped — you could be trading a heating bill for an air conditioning bill, for instance. However, differences in energy costs can also work in your favor, so it’s worth doing your research.

Austin Courrege/Bankrate

Let’s say you currently live in Connecticut, where average energy bills are among the highest in the nation — about $151 per month in 2019. If you move to New Mexico, where monthly energy bills were $80 on average, you’ll save a couple hundred dollars a year on energy alone.

Lastly, find out if HOAs are common in your target neighborhoods. If you have the community narrowed down already, find out what the monthly fees are and include those in your estimates. (While you’re at it, review all of the HOA’s rules — there could be deal-breakers, such as limits on the number of guests or a ban on renting out the property for part of the year.)

2. What’s your current financial situation?

Preparing for a move is a great reason to reassess your overall financial situation. Here are key factors to consider:

- When you plan to retire

- How much money you’ll make each month from your retirement savings

- What your current expenses are, and how much you can afford based on your expected retirement income

- Whether or not you’ll need a mortgage, which could eat up a big chunk of your monthly retirement budget

It’s important to map out different scenarios based on your expected longevity and worst-case scenarios, as this affects how much you’ll have to live on.

3. What will it cost to sell your home and buy another?

Many retirees have bought and sold property already, but it may have been a while ago for some. It’s a good idea to refresh yourself with how the process works, and all the extra expenses and fees involved:

- Realtor’s commission – The fee you’ll have to pay your Realtor is typically 4 percent to 6 percent of the sale price.

- Closing costs – Depending on the real estate market you live in, you may need to take care of some closing costs on top of your agent’s fee.

- Home inspection and repairs – Buyers want a thorough home inspection before signing on the dotted line; if any structural, electrical, or plumbing issues come up, you may have to cover those expenses.

- Mortgage payoff – If your loan has a penalty for paying it off early, you’ll have an extra expense to contend with. The sum you make from selling the home will mostly go into paying off the current mortgage.

- Capital gains tax – When you sell a home for more than you paid for it, that counts as a capital gain and might need to be reported on your federal tax return. Most homeowners are eligible to exclude up to $250,000 of profit ($500,000 for married couples filing jointly) from their main home from tax, as long as they haven’t used the tax break on another home sale within the past two years. This is where it pays to keep good records: If you invested in home renovations, these expenses could help reduce your tax.

Budgeting carefully for your downsizing can make the process much less stressful, and is especially important for seniors on a fixed income. It can be easy to lose track of all the small expenses that come with a move, but with a little diligence, you can make sure you’re spending efficiently and not get blindsided by an unexpected charge.

Planning to downsize

Moving is always a frustrating experience, so break down your plan into simpler terms. Ask yourself:

1. Will you use an agent or sell your home yourself?

Selling your home yourself entails a list of responsibilities and tasks that may delay your moving process beyond your original timeline. You’ll need to devote time to preparing your home for the market, advertising the listing, vetting buyers and hosting showings, negotiating offers, and more. In general, if you’re not a very experienced seller or well-versed in how real estate transactions work in your state, it’s best to work with a listing agent.

2. Will you be selling a car?

If you don’t do much driving, don’t want the responsibility, do want the money or have a health concern keeping you from driving, selling a car is a wise decision. Many retired couples who have two cars will sell at least one when downsizing as a way to collect some cash, free up space and save on auto insurance and maintenance.

3. How else can you pare back?

A bittersweet yet rewarding part of downsizing is getting rid of stuff you no longer need. Whether that means valuables like jewelry you no longer use or junk taking up space in your garage, let it go! If you have children, ask them what they’d like to take, and then donate or sell items you’re no longer interested in keeping. If the process of paring down seems overwhelming, consider hiring a professional organizer to help you.

4. How will you decide where to live?

If you don’t already know where you’re going to land, would you prefer to stay in the same area, or are you excited about the prospect of moving to a new place? If you’re moving somewhere new, take into consideration what you’ll need access to now and later. Check for proximity to hospitals, grocery stores and other essentials. Downsizing should make life easier — if you have to travel 45 minutes to weekly doctor appointments, think about how that will affect your quality of life.

If you’re planning to move somewhere totally new, try renting in the area for a short period of time to get a sense of whether you’d like living there in retirement. If this isn’t feasible, it’s important to at least visit the area, and ideally talk to some locals.

Keep in mind that in some parts of the country, downsizing will put you in a more competitive market, so look carefully at how much the kinds of houses you’re interested are going for.

5. What type of home do you want?

As a retiree (or soon-to-be one), you’ll want to consider downsizing to a property that will be a longer-term fit for you as you age.

- Single-family home – With a smaller single-family home, you’ll be responsible for the most upkeep, but have the most similar lifestyle if you’re moving from a larger single-family property. If you enjoy entertaining, or even activities like gardening, and like privacy, this could be the best option.

- Condo – Condos are excellent options for retired seniors who value their freedom and self-sufficiency and also want to get off the hook for property maintenance, but there can be downsides, such as HOA fees or cliquey neighbors. Make sure to evaluate the community carefully before committing.

- Assisted-living community – Assisted living communities provide housing, meal prep and health-related services for seniors. Many include luxury amenities and a more thorough level of personal care. Assisted living is an especially good option for seniors with health concerns.

- Move in with adult children – Assuming boundaries are respected on both sides, moving in with family can help ease any financial burdens you may have had in your own home and keep you close to your children and grandchildren. If there isn’t enough space, look into a “granny flat,” essentially a tiny home that can be built on your child’s property. Constructing one isn’t an easy process by any stretch, but if you’re set on living with family, it can be an alternative worth exploring.

When deciding what type of home to downsize to, consider you comfort level, as well. A much smaller home could seem like a good idea in theory, but in practice can be much more difficult to acclimate to, especially if you’re used to living in a larger space.

6. How will you shop for a new mortgage?

Downsizing to a new home in your retirement years puts you in a unique position when it comes to finding a mortgage. After selling your old home and extra assets, you could be able to apply for a loan with manageable monthly payments. Here are a few popular options:

- 10-year mortgage – One of the shortest-term mortgages and usually the one with the lowest rates, 10-year mortgages are great for those who want to quickly accrue equity in their home and pay less interest than they would with a longer mortgage. Your monthly payments will be higher than with a longer-term loan, but it can still be a good deal if your principal isn’t too high.

- 15-year mortgage – Fifteen-year terms also carry lower mortgage rates and APRs than longer-term loans, though usually not as low as with a 10-year term. If you want to get the house paid off as quickly as possible but aren’t comfortable with the monthly payment associated with a 10-year mortgage, consider a 15-year one instead. You’ll have a little more leeway in monthly spending while still being able to pay off the home relatively quickly.

- 30-year mortgage – This is the most popular kind of home loan overall, though it can be a little tricky for downsizers. The extended term means you could be paying it off throughout your retirement, and although the monthly installments will be less than a shorter-term loan, you could spend a significant chunk of your golden years paying off a new housing debt.

- Interest-only mortgage – If your income is stable, an interest-only mortgage could be a viable option, since you’ll have relatively low monthly payments with this type of loan. True, you won’t build equity because you’re not paying down the loan principal, but at this stage, you might not need it, so it’s worth exploring.

Learn more:

- Best age for Social Security retirement benefits

- Compare current refinance rates

- Estate planning checklist