Let’s take a moment to talk about “interest-only home loans.” A decade ago, very few individuals seemed to be interested in actually paying off their mortgages.

Many prospective and current homeowners alike just wanted to get the cheapest financing available, with the lowest monthly payment options, regardless of the consequences.

That meant buying real estate with 100% financing and throwing in an interest-only option on top. Oh, and these loans were typically adjustable-rate mortgages, not 30-year fixed mortgages.

However, they were available on pretty much any loan program, from a one month adjustable-rate mortgage to a 30-year fixed rate mortgage. The once popular pick-a-pay loans had an interest-only option available as well.

Jump to interest-only loan topics:

– How an Interest-Only Mortgage Works

– Pay Off Your Loan or Keep Payments Low

– Interest-Only Home Loans Eventually Adjust Higher

– You Pay for the Interest-Only Privilege

– How to Calculate an Interest-Only Mortgage

– Interest-Only Mortgage Qualification

– Pros and Cons of Interest-Only Mortgages

With so many exotic mortgage programs available, such as negative-amortization loans and loan programs with introductory teaser rates, it was easy to understand why borrowers did what they did.

In fact, interest-only options used to be almost a given on mortgages back then.

But times have changed, and these days it’s pretty uncommon to find a mortgage lender willing to give you an interest-only mortgage.

Of course, there are still lenders out there, it’s just more of a specialty now.

How an Interest-Only Mortgage Works

- You get the option to pay only interest each month

- None of your monthly payment goes toward the principal balance

- This means the loan amount doesn’t decrease

- But you can still make fully-amortized payments if you want

In a nutshell, with an interest-only mortgage you have the option to just pay the interest portion of the mortgage payment each month.

A standard mortgage payment consists of two main components: principal and interest.

The principal portion is the amount you owe (the loan amount), and the interest portion is the cost of financing what you owe. The bank isn’t lending you money for free you know.

Instead of paying principal and interest, you just pay interest each month. And that makes it significantly cheaper.

This allows a homeowner to save money and still gain equity if housing prices increase, even though their loan balance stays the same.

Let’s look at an interest-only home loan to highlight this point:

Loan amount: $400,000

Interest rate: 4%

Principal & interest payment: $1,909.66

Interest-only payment: $1,333.33

As you can see, the interest-only payment is much more attractive than the principal and interest payment, nearly $600 less each month. That’s the appeal.

Note: You still have the option of making the fully-amortized payment if you choose. The interest-only option is just that, a payment option, which is totally optional. It’s basically just added flexibility.

Do You Want to Pay Off Your Loan or Keep Payments Low?

- An interest-only mortgage is good for keeping payments low

- If you have times of the year where cash flow is limited

- The downside is you won’t be paying down the loan

- Eventually you’ll need to unless home prices rise and you sell it

But what many prospective home buyers and homeowners may not realize is that offsetting or reducing monthly mortgage payments increases the overall interest one pays over the life of the loan, and reduces the amount of home equity one will gain.

If you make interest-only payments on your mortgage each month for the first ten years, you will pay substantially less than your fully-amortized payment, but gain nothing in the way of home equity. Precious home equity…

So if you took out a mortgage with no money down, you would have zero ownership in your home unless it appreciated during that time. Meaning home prices must rise for you to gain any equity whatsoever.

If home values happened to fall during that time, you could easily find yourself in an underwater position seeing that you elected to put nothing down and pay no principal each month.

This could be a big problem if you planned on selling the home in a short period of time.

Interest-Only Home Loans Eventually Adjust Higher

- The interest-only period typically ends after 10 years

- Then you must make full mortgage payments

- Over a 20 year period (remaining loan term if 30 years)

- Which can equate to a very significant payment increase

Here’s another important warning about interest-only home loans. The interest-only period typically only lasts for the first 5-10 years of the loan, at which point your monthly mortgage payments can jump to possibly unmanageable levels.

You actually get hit twice. After the interest-only periods ends, your minimum payment converts to the fully-amortized payment (principal payments and interest).

And because the starting mortgage balance could still be fully intact after only paying the interest due each month, you’d have to pay that full loan balance in 20 years instead of 30 (assuming it’s a 30-year loan).

Hello significantly larger mortgage payment! If it’s an ARM, you could get hit three times if the interest rate also adjusts higher.

That is, unless you’re able to refinance or sell before that happens…which is what most people bank on.

But you can’t always count on lower mortgage rates in the future, and if you can’t handle the extra payment amount, beware!

Most homeowners usually just refinance once their options are exhausted, and find a new, lower payment option. And then repeat the cycle.

With home prices on the up and up, the idea is that you can eventually gain considerable ownership in your home without ever paying any money toward the principal balance.

This was the main premise of the infamous option arm. But those days seem to be well behind us now.

You Pay for the Interest-Only Privilege

- The interest-only option typically isn’t free

- Expect either a higher mortgage rate

- Or higher closing costs

- If you want this type of loan

Interest-only loans usually come at a cost too, about .125 to .25 to the fee, or perhaps .125 (1/8) to the interest rate.

So instead of an mortgage rate of 4%, you might be stuck with a rate of 4.25% if you opt for an interest-only option. Or higher closing costs. E

Put simply, you actually have to pay for the privilege to not pay down your principal balance, which seems a bit odd.

That being said, many think interest-only mortgages are a complete waste of time, and that you should always pay down at least some principal each month.

But it really depends on what you plan to do with your home, and if you see yourself owning the property outright at some point.

If it’s just an investment property, or a short-term fixer upper, you could argue in favor of making interest-only payments to keep costs low while leveraging the money elsewhere.

But if you plan on staying in your home long-term, it is generally wise to pay both principal and interest to gain ownership in your home.

How to Calculate an Interest-Only Mortgage

- It’s actually very easy to calculate since we don’t have to factor in principal

- Simply multiply the loan amount by the interest rate

- Then divide by 12 to get the monthly cost

- And voila!

This is probably one the easier mortgage calculations out there. Seriously, you don’t even need a mortgage calculator (or an interest only mortgage calculator).

All you have to do is take the interest rate, multiply it by the loan amount, and then divide that by 12 (months).

So if the rate is 4% and the loan amount is $400,000, simply input .04 and multiply it by $400,000.

That equates to $16,000, which is the annual amount of interest paid. Then divide by 12 and you get $1,333.33, which is the monthly interest-only mortgage payment.

And because the loan balance doesn’t change (go down) if you’re only making interest payments, the calculation never changes either. Easy!

Interest-Only Mortgage Qualification

- In the past lenders may have used the interest-only payment for qualifying purposes

- But that was clearly flawed seeing that the payment wasn’t fully-amortizing

- Today expect to be underwritten with the principal and interest payment

- To ensure you can manage full payments once the IO option disappears

Back in the day, it may have been easy for home buyers to qualify for an interest-only loan. Not anymore.

Lenders wised up and realized that they couldn’t qualify someone using the lowest payment possible and ignore the higher payment looming on the horizon.

Thus, they tend to qualify borrowers at the higher of the start rate +2% or the fully-indexed rate.

For example, if your 7/1 interest-only loan has a start rate of 3.75%, you’ll need to qualify at a rate of 5.75% or even higher, depending on the fully-indexed rate.

Additionally, the lender may use a monthly payment based on a 20-year amortization, which would be the remaining period after the typical 10-year IO portion.

Imagine the loan amount is $400,000 and the start rate is 3.75%. That would equate to an interest-only payment of $1,250.

Now if we pretend the fully-indexed rate is 6%, the qualifying payment would be a much higher $2,865.72 based on a 20-year term.

It just got a lot harder to qualify for the mortgage because that payment will shoot your DTI ratio up a lot higher.

In other words, you have to make a decent amount of money to qualify for these types of loans. They don’t allow you to borrow more.

Lastly, note that interest-only options are only available on certain types of mortgages.

They are commonly found on jumbo mortgages, but not available on government loan programs like FHA mortgages or VA loans, or even loans backed by Fannie Mae and Freddie Mac.

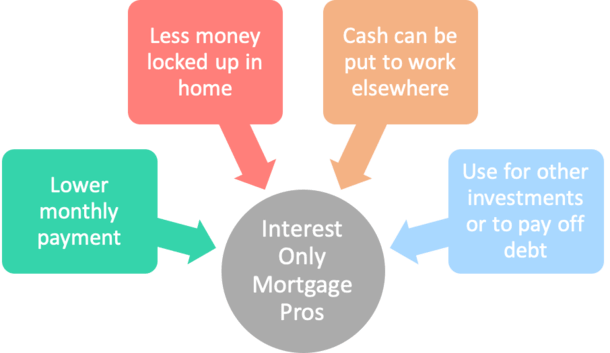

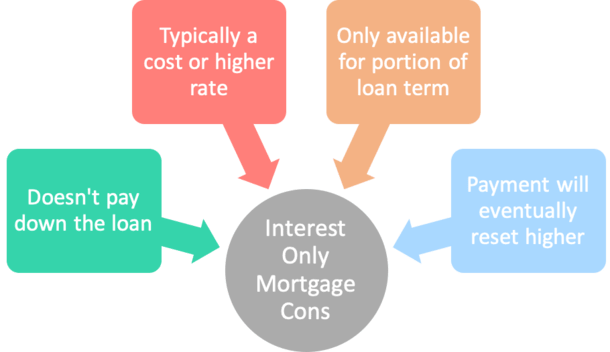

Pros and Cons of Interest-Only Mortgages

Benefits of interest-only mortgages

- Smaller monthly mortgage payment

- More affordable if money is tight (improved cash flow)

- You can buy a bigger/more expensive home today

- Excess cash each month can be used for other higher-yielding investments, retirement, Roth IRA, etc.

- Or to pay off student loans, credit cards, personal loans, etc.

- Less money locked up in an illiquid asset

- You can still build equity if home prices rise over time

Disadvantages of interest-only mortgages

- None of the monthly payment goes toward principal

- You typically must pay a cost or take on a higher interest rate for the IO option

- You can land in an underwater position pretty easily

- The interest-only period is temporary

- You will need to refinance, sell, or make larger payments in the future

- Harder to sell/refinance with little or no equity

- Doesn’t really work without home price appreciation