A “HELOC” or “home equity line of credit,” is a type of home loan that allows a borrower to open up a line of credit using their home equity as collateral. They can then draw upon it to pay for anything they wish, such as to pay off credit card debt or student loans.

Jump to HELOC topics:

– What Is a HELOC?

– Accessing Your Funds with a HELOC

– HELOC Interest Rates

– Downsides of Home Equity Lines of Credit

– Term of a Home Equity Line of Credit

– Can You Refinance a HELOC?

– Types of HELOCs

– Home Equity Line of Credit vs. Home Equity Loan

– Common HELOC Fees

– HELOC Pros and Cons

What Is a HELOC?

- A home loan with a twist because it’s actually a line of credit (as opposed to a set loan amount)

- Your property acts as collateral for the loan similar to a traditional mortgage

- Can draw upon it when needed like a credit card, which could be many times over the loan term

- Or never touch it (some homeowners simply open one as an emergency fund)

A HELOC, while also backed by real property, differs from a traditional home loan for several different reasons.

The main difference is that a HELOC is simply a line of credit a homeowner can draw from, up to a pre-determined amount set by the mortgage lender, based on the value of your home.

Conversely, with a typical mortgage, the amount borrowed is the total amount financed.

In other words, a HELOC is a lot like a credit card because of its revolving balance nature. When you open a credit card, the bank sets a certain credit limit, say $10,000.

You don’t need to pay interest on the total amount, or even withdraw or spend any of the $10,000, but it is available if and when you need it.

That’s also how a HELOC works. Your bank or lender will give you a line of credit for a certain amount, say $100,000, depending on the available equity in your home.

And you can draw upon it as much or as little as you’d like, up to that $100,000 limit, if and when you want.

Generally, you will be required to make an initial minimum draw, say $10,000 or $25,000, depending on the total line amount.

This ensures the bank actually makes money on the transaction, and doesn’t just give you a line of credit you never touch. That would be a big waste of money for them.

Once you take your initial draw, you can put it in your bank account to use for certain expenses, borrow even more, pay it back, and then borrow again. Or never touch it and just set it aside for a rainy day.

Additionally, most HELOCs allow you to make just the interest-only payment, instead of having to pay back the principal balance.

This keeps monthly payments low while also giving homeowners access to much needed cash if and when they need it.

It’s a flexible choice because you get the option to use the line of credit if you need it, without having to pay interest on it if you don’t.

With a typical mortgage refinance, you pay interest on the total loan amount from the get-go, even if the money just sits in your bank account.

Most people use the HELOC funds to pay for things like paying for college tuition, home improvements, and higher-interest rate debt like credit cards (debt consolidation).

Or to cover a down payment on another home purchase (instead of raiding their Roth IRA).

Accessing Your Funds with a HELOC

- You may be given an access card (like an ATM/credit card)

- An option to transfer funds online to your bank account

- A physical checkbook where you can write checks

- Or a bill pay option to make specific payments

Once your HELOC is open, you’ll have a variety of options to access the funds up to your pre-determined credit limit.

Most banks and mortgage lenders will provide you with an access card that works kind of like an ATM debit/credit card. You can make purchases with it and/or withdraw cash at a branch location.

You may also be given the option to transfer funds to a linked bank account, or be given checks that can be written to anyone for any purpose, which are deducted from your credit line.

There may be a bill pay option if you want to use the funds to pay bills, or an option to transfer funds over the phone or via mobile banking.

In any case, it should be pretty easy and convenient (and usually free) to access your money.

Interest Rate on a Home Equity Line of Credit

- HELOC rates are always variable

- Because they are tied to the prime rate

- To figure out your interest rate

- Simply add up your margin and the current prime rate

Now let’s talk about mortgage rates. A HELOC’s interest rate is determined by the prime rate plus the margin designated by the bank or lender.

The margin, which can vary from bank to bank, is typically fixed throughout the loan term.

And as you may already know, the prime rate is variable and can change whenever the Fed makes a monetary policy decision.

Many banks will offer HELOC rates to borrowers at the prime rate with zero margin, or even less than prime, at least initially.

You’ll often see bank ads that say “prime -1%” or something to that effect. Of course, this is usually an introductory rate, and will often go up after the first few months or year once the rate discounts no longer apply.

When reviewing HELOC rates, you’ll likely see the annual percentage rate (APR) listed alongside it, along with the word “variable,” because as noted, it’s tied to prime, which can change whenever the Fed decides to raise or lower rates.

Like mortgage rates on a normal home loan, your credit history will come into play in determining your HELOC rate, so strive for excellent credit to obtain the lowest rate.

Your loan-to-value ratio is also quite important, so the more equity in your home, the better. Put simply, a lower LTV, or CLTV as it’s known if the HELOC is a second mortgage, is key to a low HELOC rate.

Along some same lines, lower loan amounts might come with slightly cheaper rates, and you might be required to order a home appraisal over certain loan amount thresholds.

Like any mortgage you shop for, be sure to compare rates to ensure you don’t miss out on a good deal.

HELOC promos vary widely from bank to bank. Credit unions often offer great deals, and should be on your list of places to shop.

After the promo period ends, expect a margin greater than zero plus prime.

For example, you might see something like prime + 2%. Prime is currently 4.50%, so the fully-indexed rate would be 6.50%. A well-qualified borrower may get a rate as low as prime + 0.5%.

If your loan scenario is a bit more high-risk, it could carry a margin of 4% or more, which when combined with the prime rate, can be quite hefty.

That would make the interest rate 8.50%, which isn’t a very desirable rate.

When shopping for a HELOC, pay close attention to the margin since it’s the one number that you can control. The prime rate is the same for everyone.

Tip: Ask for the margin during the draw period and the repayment period. Sometimes lenders will impose a higher margin during the latter period, which can get expensive!

Downsides of Home Equity Lines of Credit

- The rate is adjustable and tied to prime

- It can go up significantly during periods of inflation

- Rate adjustments can be frequent relative to other ARMs

- Higher interest rate caps

Many borrowers steer clear of HELOCs for a number of reasons. The main reason being that a HELOC is an adjustable-rate mortgage, tied to prime.

Whenever the Fed moves the prime rate, the rate on your HELOC will change.

Usually it’s only .25% at a time, but the Fed raised the prime rate about 20 times in a row since 2004, pushing the rate from 4% to 8.25%, before it began to move the other way.

So your interest rate can fluctuate greatly, even if the Fed moves prime in so-called “measured” amounts.

HELOCs generally adjust either monthly or quarterly, depending on the terms specified by the lender.

Check your paperwork so you know what to expect after the Fed makes a move.

Also note that HELOCs don’t have periodic interest rate caps like standard adjustable-rate mortgages, just lifetime caps, so the rate can fluctuate as much as the Fed allows it to, up to 18% in California (it varies by state).

Term of a Home Equity Line of Credit

- Typically begins with a 5-10 year draw period

- Where you can make interest-only payments each month

- Followed by a 10-20 year repayment period

- Where you must pay back principal and interest to satisfy the loan

A HELOC normally has a 25-year term, with a draw period and a repayment period. The draw is typically the first 5 to 10 years, followed by the repayment period of 10 to 20 years.

But it can vary, with some HELOCs offering 20 year draws and 20 year repayment periods to lessen the payment burden.

During the draw period, the homeowner can borrow as much as they’d like within the line amount, and can make interest-only payments on the amount drawn upon.

There is usually a minimum payment, just like a credit card.

After the draw period, the borrower must pay off the principal of the HELOC, along with the interest. This period is known as the repayment period.

Usually the loan balance is broken down into monthly payments, but there could also be a balloon payment because of the way the loan amortizes.

Also note that some HELOCs don’t have a repayment period, so full payment is simply due at the end of the draw period.

Can You Refinance a HELOC?

- It’s possible to refinance a HELOC like any other home loan

- The most common method is a cash out refinance that combines your first mortgage and home equity line

- Another option is to take out a new HELOC that pays off the old HELOC

- Or pay off the HELOC with a home equity loan instead

Now you might be wondering if it’s possible to refinance a HELOC, especially if the draw period has come to an end and the repayment period is in effect.

If you were used to making interest-only payments, then all of a sudden have to make fully-amortized payments over a shorter remaining term, it can get expensive.

In fact, your HELOC’s monthly payment could jump by a few hundred bucks depending on the interest rate and loan amount.

The good news is it is possible to refinance your HELOC, just like your first mortgage.

The most common way to extinguish a HELOC is to pay it off via a cash out refinance, combining your first mortgage and second mortgage, which is the home equity line.

FYI, it’s considered cash out because you’re paying off a non-purchase money loan.

Let’s look at a quick example:

Home value: $500,000

First mortgage (outstanding balance): $300,000

HELOC (outstanding balance): $65,000

In this common scenario, you’d have total outstanding liens of $365,000 on a property valued at $500,000.

That would put your LTV ratio at 73%, which leaves plenty of equity to take advantage of a refinance.

If interest rates were favorable at the time of refinance, you could ideally get a new blended interest rate that saves you money each month.

And since HELOCs are variable-rate, you could fix your interest rate at the same time.

Best of all, you’d have just one mortgage again, instead of two.

Now if mortgage rates aren’t great and you want to refinance your HELOC, you could look into simply getting a new HELOC to replace the old one.

Again, you’ll want to ensure you have sufficient equity in your home to allow for a new HELOC. And the new financing should make sense, aka a cheaper payment or lower rate.

Another option is to pay off your HELOC with a home equity loan, the latter of which comes with a fixed interest rate and loan amount, as opposed to a variable rate and revolving balance.

This might be attractive if the fixed rate is relatively low, though you may want to compare loan costs to a standard refinance.

Finally, some lenders will offer the option to switch from a variable rate to a fixed rate on all or some of your outstanding line of credit. This might be another way to avoid higher costs if the prime rate keeps increasing.

But ultimately, a standard refinance is generally the way to go in most cases because interest rates tend to be a lot lower on first mortgages.

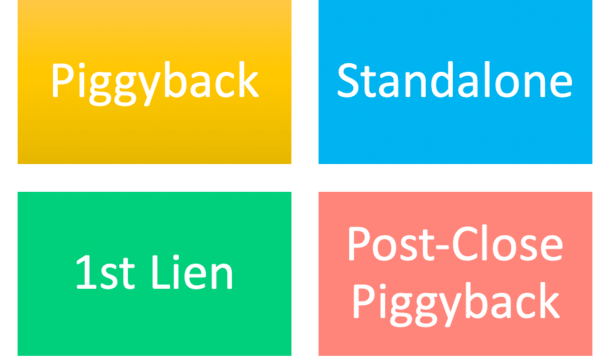

Types of HELOCs

- HELOCs are often utilized as piggyback second mortgages

- These extend financing if you don’t have sufficient down payment funds

- Can also be used as a non-purchase money second mortgage after you close on your first mortgage

- They are also less commonly taken out as first-lien mortgages

Most HELOCs are opened behind an existing first mortgage as a source of funds to pay down credit cards or other revolving debt, or for home improvements and other household costs.

These are known as standalone HELOCs, which provide flexibility at a relatively low interest-rate compared to a standard credit card or other means of financing.

They can also be used as purchase-money second mortgages (piggyback) to extend financing and allow a homeowner to put less money down on a home purchase.

In this fairly common scenario, the HELOC utilizes the entire credit line as the down payment, and the borrower must pay interest on the full amount from day one.

For example, if a borrower wanted a zero-down mortgage on a $100,000 property, they could open an $80,000 first mortgage for 80% LTV and a second mortgage (the HELOC) to cover the remaining $20,000, or 20%.

Another option might be a post-close piggyback where a HELOC is opened shortly after loan closing to boost liquidity if the homeowner used the funds to plunk down a larger down payment, perhaps to win a bidding war.

Lastly, some borrowers may even open a HELOC as a first mortgage, although it is less common and can be somewhat risky for a homeowner if the prime rate rises rapidly, which it has been known to do in times when inflation is high.

Home Equity Line of Credit vs. Home Equity Loan

- A HELOC is adjustable

- And you’re given a line amount similar to a credit card

- A home equity loan is generally fixed

- And the loan amount is the amount borrowed from day one

If you’ve been shopping for a HELOC, you may have come across a home equity loan as well. They aren’t the same.

With a home equity loan, you receive the full lump sum and make monthly mortgage payments on that total amount of borrowed money immediately, usually at a fixed rate.

A HELOC, on the other hand, not only gives the borrower the freedom to decide when and if to use the money, but also how much they need to pay back and when.

In a sense, it might be a good alternative to a reverse mortgage because it provides cash if and when needed, with no payments if it’s not accessed.

Borrowers generally choose HELOCs as purchase-money second mortgages because the interest rate and payment is lower than closed-end fixed home equity loans.

And HELOCs have an interest-only option which many fixed-end seconds don’t offer. HELOCs also don’t carry prepayment penalties, whereas many fixed-end seconds do.

Once the borrower pays down the HELOC, they also have the option to draw upon it again if they need additional funds, something a home equity loan doesn’t offer.

With a home equity loan, it’s a one-time use that must be paid back over a set period of time, just like a traditional home loan.

Common HELOC Fees

- You may have to pay closing costs with a HELOC

- Similar to a standard mortgage

- But in most cases they’re free to open

- Just watch out for annual fees and early closure fees!

Another negative to HELOCs are the associated fees. Some of them require you to order an appraisal, which can amount to several hundred dollars. Others will charge closing costs and an origination fee.

There may also be an annual fee on your HELOC, which could range from $50 to $100 or more per year. Over time that can add up.

HELOCs also tend to come with early closure fees of around $300-$500, although they don’t usually carry an explicit prepayment penalty.

This means if you close your equity line just 1-3 years into the loan, the bank will charge this fee. Again, they want to make money off the deal, so if you close the line too quickly, they’ll probably charge you for it.

Sometimes the fee will be equivalent to what they would have charged for closing costs.

For example, they may say you can get a HELOC without closing costs, but charge you those fees later if the line isn’t kept open for a minimum period of time.

HELOC Pros and Cons

HELOC advantages:

– lower interest rate than a fixed home equity loan

– easy to access funds

– interest-only option

– usually no prepayment penalty

– ability to choose draw amount you want, when you want

– don’t need to borrow more than you need and pay interest on it

– able to borrow multiple times from same credit line

– lower or no closing costs

HELOC disadvantages:

– adjustable interest rate tied to prime

– no periodic caps on interest rate

– rate can adjust much higher over time

– early closure fees may be applicable

– minimum draw amounts with some lenders

– annual fees may apply